Industry Overview:

The global insurance market was valued at $8.6 trillion in 2022 and is anticipated to grow at a CAGR of 1.97% in the forecast period (2022-2028) to reach nearly 10 trillion by 2028

Technological Trends

New models, personalized products

Usage-based, on-demand, and "all-in-one" insurance lifestyle solutions will become increasingly relevant in the digital economy; consumers will favor customized insurance policies over the existing one-size-fits-all offerings; flexible coverage is viable in the long run

AI & Automation for faster claims

- Insurance will see a significant rise in robotic process automation (RPA) and AI, thanks to improved data processing capabilities, novel data channels & AI algorithm developments

- Tyche, another InsurTech company, uses an AI-powered claim likelihood model in underwriting to precisely assess risks and increase profitability

Advanced Analytics & Proactiveness

- Because of emerging tech-enabled data sources like wearables, mobile-enabled InsurTech apps, and the Internet of Things, premiums will become much more tailored.

- To dynamically segment consumers and needs, model behaviors and discover exceptions, modify policy rates, optimize business strategies, and spot new growth prospects, advanced analytics will be implemented

Industry Outlook

Opportunities:

Cyber Insurance

The demand for insurance solutions covering ransomware attacks, data breaches, and other cyber incidents—with extended options to include business interruptions—is growing as cyber risks escalate

Personalized Insurance

Implementing in place usage-and behavior-based pricing models and providing customized rates based on unique risk profiles for home, health, and vehicle insurance with dynamic policies to adjust coverage level & duration based needs

Insurtech and Digital Innovation

Using AI and machine learning to improve customer service (chatbots), fraud detection, predictive analytics, and targeted marketing creating internet portals and smartphone apps to facilitate customer support, submitting claims etc.

Regulatory and Policy Changes

Creating goods and services to assist companies in adhering to new rules such as data protection laws and working with governments to create public-private alliances for social insurance and catastrophe risk management

Regional Insights-India:

Risks in the Industry:

Cybersecurity and Data security threats

Financial losses, reputational harm, legal ramifications, regulatory fines, and data breaches are all possible outcomes of cyberattacks and data breaches. Because hackers have the ability to steal critical data, there is a high stakes in preventing cyber dangers

The increase in nominal interest rates

Global insurance rates are at an all-time high; although certain life insurance businesses may take advantage of this for short-term financial benefits, in the long run, this raises borrowing costs and reduces long-term profit margins

Inflation and the impact on replacement and other costs

As a percentage of income, costs have risen by 23% since 2003, but P&C insurers' prices have decreased significantly; these expenses will only rise in line with inflation, and rising premiums may lead to an increase in client recidivism in lean economic times

Climate change and sustainability

The existing regulatory obligations pertaining to climate change are likely to worsen, and insurers may have challenges in assessing and pricing climate-related risks, as well as greater claims payouts and increasing reinsurance costs

1. Industry Overview

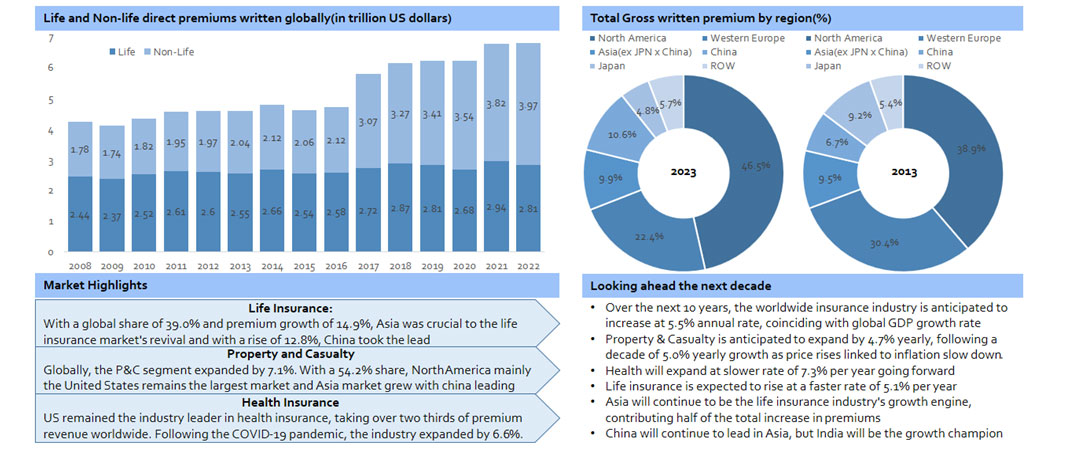

- 1.1. Life and Non-life direct premiums written globally(in trillion US dollars)

- 1.2. Total gross premium by region (%)

- 1.3. Looking ahead the next decade

- 1.4. Market highlights

2. Industry Market Size

- 2.1. Value of gross written premiums worldwide(in trillion US dollars)

- 2.2. Global insurance market share

- 2.3. Cyber insurance market size(in billion US dollars)

- 2.4. Global insurance market dynamics

3. Industry Outlook

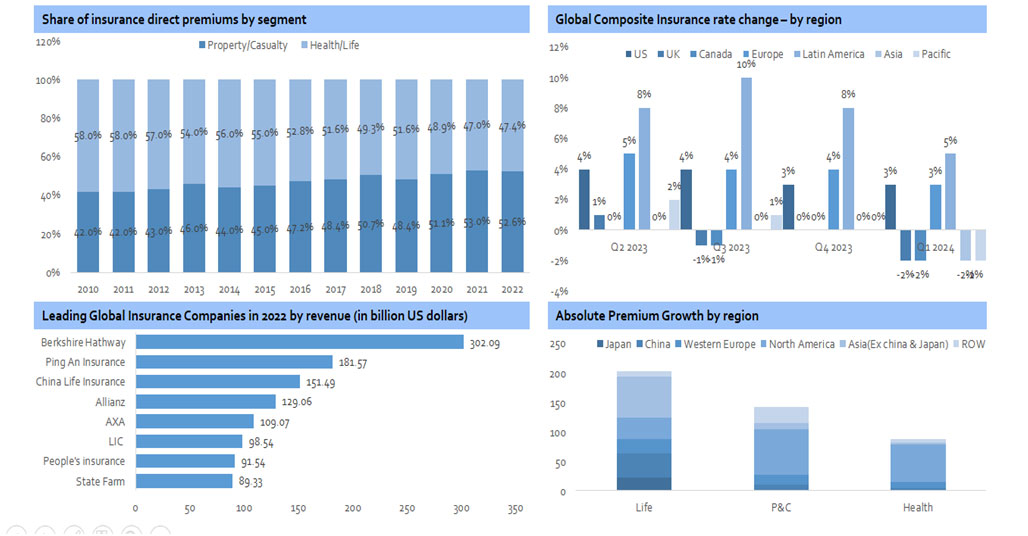

- 3.1. Share of insurance direct premiums by segment

- 3.2. Global composite insurance rate change by region

- 3.3. Absolute premium growth by region

- 3.4. Leading global insurance companies in 2022 by region

4. Industry Trends

- 4.1. Technological trends

- 4.2. Incorporating sustainability into operations

- 4.3. Global product line trends

5. Pricing Insights

- 5.1. Change in commercial insurance pricing, worldwide

- 5.2. Premium inflation for health insurance

- 5.3. Pricing types

- 5.4. Global insurance premiums

6. Consumer Insights

- 6.1. Investment attitude of consumers by region

- 6.2. Preference and potential purchase of policies, 2023

- 6.3. Consumer & SME’s restraints from buying or renew insurance

- 6.4. Concerns for having insurance

7. Opportunities & Challenges

- 7.1. Opportunities

- 7.2. Challenges

- 7.3. Top challenges for the life insurance companies

- 7.4. Themes defining the near future of insurance

8. Risk and Mitigation

- 8.1. Risks prevailing in the industry

- 8.2. Risks Mitigation

- 8.3. Fraud management techniques adopted by insurer

- 8.4. Reasons attributed for fraud

9. Global Insurance Developments

10. Competitive Benchmarking

11. Company Analysis(1/3)

- 11.1. Revenue of Allianz group

- 11.2. Distribution of third party assets by region,2023

- 11.3. Strategic areas of focus

- 11.4. Allocated risks as per risk profile

12. Company Analysis(2/3)

- 12.1. Financial Highlights

- 12.2. Revenue by geographic regions

- 12.3. Strategic focus for the future

- 12.4. Growth across main lines of business

13. Company Analysis (3/3)

- 13.1. Gross written premium by segment

- 13.2. Total gross written premium by country,2023

- 13.3. Strategic Pillars of growth

- 13.4. Key Facts

14. Regional Insights-USA

- 14.1. Insurance sector market size

- 14.2. Direct written premiums by state

- 14.3. Major players

- 14.4. Direct earned health premiums and deposits by sector

- 14.5. Net written premium

15. Regional Insights-India

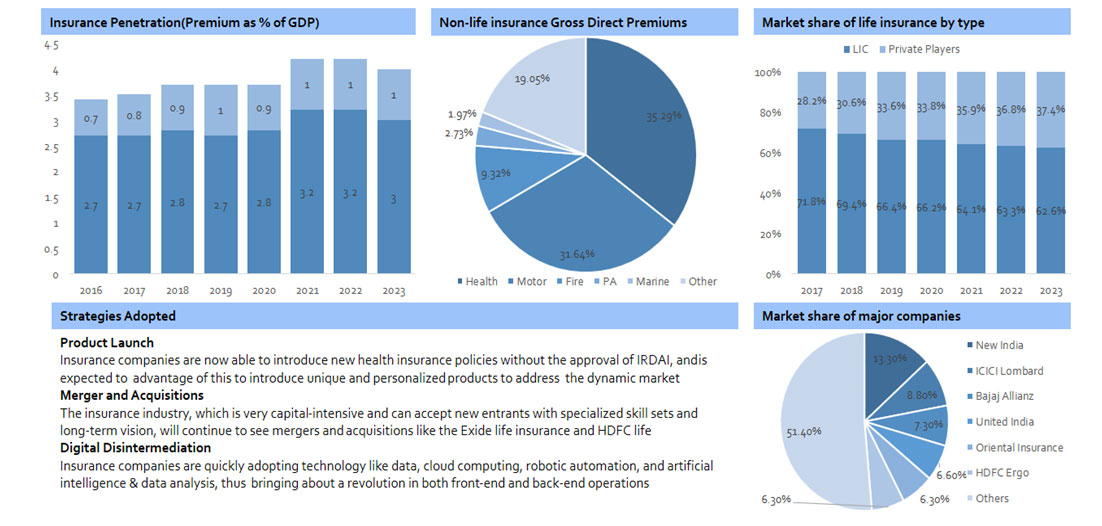

- 15.1. Insurance penetration

- 15.2. Non-life insurance gross direct premiums

- 15.3. Market share of life insurance by type

- 15.4. Strategies adopted

- 15.5. Market share of major companies

16. Regional Insights-United Kingdom

- 16.1. Gross written premium by personal lines

- 16.2. Household expenditure on life insurance

- 16.3. Major players

- 16.4. Gross written premium by commercial lines

- 16.5. Sectors on note

17. PORTER’S Analysis

18. SWOT Analysis